Brazil

Company Law and Climate Change

You are viewing part of the Law and Climate Atlas

Introduction

According to the Brazilian constitutional and legal regime, business activity must observe a social function that includes the duty to consider environmental and climate impacts in its decisions.

In this context, the Brazilian Securities and Exchange Commission (“CVM”) has been bringing regulatory advances that drive the integration of environmental, social, and governance factors (“ESG”) factors into corporate governance, with emphasis on the adoption of international standards IFRS S1 and S2 as methodologies for the disclosure of mandatory information by publicly-held companies. Brazilian companies are also subject to indirect impacts resulting from regulatory measures implemented in the financial system by the Central Bank of Brazil (“BCB”) – such as access to financing and credit lines, for example.

In addition, Brazil also has emblematic cases of climate litigation against companies, including civil liability actions for climate damage and questions about possible climate-washing practices. These cases demonstrate the growing role of the Judiciary and civil society in monitoring business practices and consolidating a robust climate legal regime that is consistent with the country’s international commitments.

The CVM has promoted the integration of ESG factors into the capital market, with emphasis on the adoption of IFRS S1 and S2 standards and the mandatory nature of sustainability reports as of 2026.

Among the cases of climate litigation against companies in Brazil, it is possible to identify a trend in cases with requests for reparation of climate damages, questions of climate-washing, and questioning of investment policies of financial institutions based on alleged violations of fiduciary duties and the social function of companies as provided by the Brazilian Corporations Act.

Brazilian business law and climate change

As established by the Federal Constitution of Brazil[1], the economic order must observe a series of principles (Article 170). Among them are national sovereignty, private property, the social function of property and the protection of the environment. Thus, according to the guideline present in item VI of Article 170 of the Federal Constitution[2], the company’s function goes beyond generating profit and must consider the protection of the environment.

In addition, the Federal Supreme Court (“STF”) understood, within the scope of the Allegation of Non-Compliance with a Fundamental Precept No. 708 (“ADPF 708”)[3], that the climate is constitutionally protected by Brazilian Law, since climate is considered part of the constitutionally protected ecologically balanced environment, guaranteed by Article 225 of the Constitution[4].

It is worth noting that the company’s social function is also expressly provided for in the “Brazilian Corporation Act” (Law No. 6,404/76, Article 116, sole paragraph, and Article 154, paragraph 1),[5] which determines that the manager must exercise his duties “in the interest of the company, meeting the requirements of the public good and the social function of the company”.

This principle has become especially relevant in the context of climate change, as it imposes on companies – especially publicly-held companies – the duty to consider, in the exercise of their economic activity, the socio-environmental impacts of their decisions. Thus, the Brazilian regime is open to a review of the classic interpretation of the primacy of shareholder value[6] in light of corporate responsibility towards stakeholders and the community, which includes the management of climate risks and the promotion of business practices aligned with the transition to a low-carbon economy. Further, Brazilian environmental law, among other areas, includes exceptions to limited liability in some circumstances, allowing courts to ‘pierce the corporate veil’ and potentially hold owners more directly to account for climate-related damages.[7]

The sixth edition of the Code of Best Corporate Governance Practices of the Brazilian Institute of Corporate Governance (“IBGC”) stands out, which now expressly includes sustainability as one of the fundamental principles of corporate governance, reinforcing the role of companies in generating long-term value and considering the social and environmental impacts of their activities.

Notably, CVM reformulated the structure of the Reference Form through CVM Resolution No. 59, of December 22, 2021, requiring the disclosure of information on ESG aspects in the document.

Although the CVM’s regulation focuses on publicly-held (listed) companies, it is important to note that the provisions of Brazilian Corporations Act apply to closely-held (unlisted) companies[8]. Thus, the principles of the social function of the company, socio-environmental responsibility and sustainable governance have implications for all companies (sociedade por ações), reinforcing the need to align business practices with the sustainable development goals and the transition to a low-carbon economy.

Business performance, therefore, is an essential instrument for mitigating climate change, since business entities are responsible for a large part of greenhouse gas (“GHG”) emissions around the world. By incorporating climate (and ESG) criteria into corporate governance, companies can contribute significantly to tackling climate change and its adverse effects – in addition to contributing to the fulfillment of Brazil’s climate commitments. In August 2025, the Interinstitutional Committee of the “Brazilian Sustainable Taxonomy” approved final rules for a ‘green taxonomy’ which will operate in Brazil. Like similar taxonomies developed in other jurisdictions, this would classify economic activities based on environmental impacts. Once implemented, this may give investors better information about climate-related risks and opportunities associated with their investments, and companies scope to attract investment based on their environmental credentials.

In November 2025, the Brazilian Sustainable Taxonomy was formally enacted through Federal Decree No. 12,075/2025[9], and its classification system for economic activities, assets, and project associated to ESG objectives was finally introduced. Regarding applicable criteria, to be considered sustainable an activity must (i) make a substantial positive contribution to one or more objectives, (ii) avoid significant harm to others, and (iii) comply with minimum safeguards and legal standards (Article 6, I, II and III, Federal Decree No. 12,075/2025). The classification of assets, activities, and project categories under the Brazil Sustainable Taxonomy will be carried out individually, by organization or enterprise, in a way that allows verification of compliance with the established criteria (Article 6º, §7º, Federal Decree No. 12,075/2025).

Climate obligations in Brazilian business law

Based on these premises, the Brazilian regime assigns climate obligations to companies mainly regarding the disclosure of information from publicly-held companies, emission reduction obligations within the scope of the Brazilian carbon compliance market (“SBCE”) and specific obligations regarding the control of environmental compliance in the value chain associated with products and services.

Climate information disclosure

In recent years, CVM has made significant progress in the integration of ESG to the regulatory framework for publicly-held companies in Brazil. Recent reforms focus mainly on disclosure obligations for publicly-held companies, with an increasing focus on managing climate-related risks and opportunities. The regulatory development demonstrates a clear path: from a voluntary disclosure or “practice or explain” model to a mandatory financial climate reporting structure, aligned with international sustainability standards (IFRS S1[10] and S2[11]) issued by the International Sustainability Standards Board (“ISSB”) and incorporated into the Brazilian regulatory system through CVM Resolutions No. 217/2024[12] and 218/2024[13].

CVM Resolution No. 59[14], published in December 2021, represented a milestone by incorporating specific information requirements on ESG aspects into the Reference Form, the main instrument for continuous disclosure of publicly-held companies in Brazil. The rule amended CVM Instruction No. 80, which now requires, as of 2023, that companies inform whether they disclose sustainability or ESG reports (Annex C – Item 1.9). If so, they must indicate: (i) the standard or methodology used; (ii) whether the report was audited by an independent third party; (iii) the main ESG indicators disclosed; and (iv) whether there is alignment with the UN Sustainable Development Goals (“SDGs”), with the recommendations of the TCFD (Task Force on Climate-related Financial Disclosures) or financial disclosure recommendations of other recognized entities that are related to climate issues.

In addition, CVM Resolution No. 59 introduced climate risks as a specific category in Item 4 of the Reference Form, requiring companies to describe physical risks (such as extreme events, sea level rise, among others) and transition risks (arising from regulatory, technological and market changes associated with the transition to a low-carbon economy). Item 7.1 also requires companies to report on the role of management bodies in assessing, managing, and supervising climate-related risks and opportunities, reinforcing the responsibility of corporate governance in conducting strategies aligned with sustainability and climate resilience.

Although it still adopts the “comply or explain” model, the rule established the regulatory expectation around ESG transparency, making it an integral part of the informational regime of the Brazilian capital market.

CVM Resolution No. 193[15], as amended by CVM Resolutions No. 217[16], 218[17], 219[18] and 227[19], established the basis for the disclosure of financial information related to sustainability, initially on a voluntary basis and, as of 2026, on a mandatory basis. Publicly-held companies, investment funds and securitization companies may (and publicly-held companies must, as of the fiscal years started on or after January 1, 2026) (Article 2) prepare an annual report based on the international standards IFRS S1 and IFRS S2, issued by the ISSB (Article 1) and internalized in Brazil through CBPS Technical Pronouncements No. 01 and No. 02[20]. According to João Pedro Nascimento, president of the CVM at the time of the publication of Resolution 193, Brazil became the first country in the world to officially incorporate these standards into its regulatory framework, demonstrating CVM’s commitment to contributing to the achievement of the SDGs of the UN 2030 Agenda[21].

The report must be disclosed separately from the conventional financial statements and requires communication to the market (Article 1, §2 and Article 4, §1)). In addition, CVM Resolution No. 193 establishes that the report of financial information related to sustainability must be submitted to an independent auditor registered with the CVM, in accordance with the rules issued by the Federal Accounting Council (“CFC”) (Article 6), with limited required until the end of fiscal year 2025, and reasonable assurance from 2026 onwards, requiring a more rigorous process by auditors.

In voluntary adoption exercises, the report must be disclosed by the last day of the ninth month after the end of the year (Article 5, I). For the first year of mandatory adoption, the report must be released on the same date as the Reference Form (Article 5, II). From the second fiscal year of mandatory adoption, the report must be disclosed within three months after the end of the fiscal year or on the same date as the financial statements, whichever occurs first (Article 5, III).

Brazilian companies have already expressed the early adoption of the standards voluntarily: reports along the lines of CVM Resolution No. 193 were released on an experimental basis by companies in the mining and retail sector, which were pioneers in the adoption of IFRS S1 and S2 standards before they became mandatory. A survey by the Brazilian Association of Publicly-Held Companies (Abrasca) pointed out that about 28% of publicly-held companies intend to publish their first reports in accordance with ISSB standards between 2025 and 2026[22].

Reduction of GHG emissions

Law No. 15,042/2024[23] establishes the SBCE, the Brazilian carbon compliance market that will operate according to the cap-and-trade model. Although it is not yet operational, entities regulated by the SBCE will be subject to the obligations to monitor, disclose and demonstrate compliance with the environmental commitments defined in the National Allocation Plan. This must be done through the ownership of SBCE assets in an amount equivalent to their net emissions — either via Brazilian Emissions Quotas (CBEs), which serve as the SBCE’s allowances, or through Verified Emission Reduction or Removal Certificates (CRVEs).

The SBCE adopts an emissions threshold criterion to determine the scope of regulated entities based on their annual emissions. Accordingly, companies in all sectors are subject to SBCE obligations (except primary agriculture – Article 1, paragraph 2 and waste and effluents disposal facilities, when demonstrably adopting systems and technologies for the neutralization of their emissions – Article 30, paragraph 3) if they reach the following emission levels: (a) above 10,000 tCO2e/year and (b) above 25,000 tons of tCO2e/year (Article 30). Companies in scope (a) are subject to submit a monitoring plan and report of emissions and removals to the SBCE regulatory body; while the companies that are part of scope (b) must submit a report demonstrating that their GHG emissions are compatible with the CBEs or SBCEs they have – while also fulfilling the obligations applicable to category (a) (Article 29).

It is worth noting, however, that the SBCE is not yet in operation. In fact, as provided for in the legislation, the SBCE will be implemented through five phases (Article 50), so that, at first (Phases II and III), regulated entities will only be subject to the obligations of monitoring and disclosure of information; while the obligation to demonstrate compliance with the environmental commitments defined in the National Allocation Plan will come into force from Phase IV.

Risk management and disclosure (financial institutions)

It is also worth mentioning Brazilian regulatory framework regarding financial institutions, since Brazilian Central Bank (“BCB”) and National Monetary Counsil (“CMN”) introduced specific rules addressing social, environmental, and climate-related risks. In this sense, it is also possible to consider that these normative acts impact directly companies that qualify as financial institutions and indirectly to non-financial companies, mainly through their ability to access financing and credit lines. Furthermore, given the complexity of Brazilian financial law, this section provides only a brief overview and does not aim to be exhaustive – the subject would merit a dedicated chapter for a more detailed analysis.

Then, regarding CMN Resolution No. 4,943/2021[24] provisions, financial institutions are required to incorporate environmental, climate, and social risks into their risk management and capital management frameworks, as well as their disclosure policies. CMN Resolution No. 4,945/2021[25] also complements this by mandating socio-environmental responsibility policies, ensuring that sustainability principles are embedded in business strategies. In addition, BCB Resolution No. 139/2021[26] establishes the obligation to publish a Social, Environmental, and Climate Risk and Opportunity Report, promoting transparency and accountability in the sector.

To standardize reporting practices, BCB Normative Instruction No. 153/2021[27] introduced specific tables for the preparation of this report, while BCB Resolution No. 151/2021[28] governs the submission of related information to the Central Bank. Together, these measures reinforce the integration of ESG and climate considerations into the financial system.

Climate litigation against companies in Brazil

Scopes of liability for environmental damage

According to the Brazilian regime of environmental law, the scopes of liability are independent, so that the violation of environmental law and the configuration of environmental damage can simultaneously result in administrative sanctions, criminal sanctions and civil liability for the reparation of damages (Article 225, paragraph 3, Federal Constitution).

Administrative liability arises from an action or omission of the agent, who has acted with intent (free intention to produce the result) or fault (lack of necessary objective care, characterized by negligence, recklessness or malpractice) and which results in the violation of any rule of preservation, protection or regulation of the environment, regardless of the actual occurrence of environmental damage.

In the criminal scope, the Environmental Crimes Law (Law No. 9,605/1998)[29] subjects to its effects any person, individual or legal entity, who contributes to the practice of the typified conducts considered harmful to the environment, and it is also necessary to prove intent or guilt.

Finally, as for the civil scope, as established by Article 14, paragraph 1, of Law No. 6,938/1981 (National Environmental Policy – “PNMA”),[30] civil liability for environmental damage is objective, i.e., it does not depend on fault, and it is sufficient to prove the damage and its causal link with the activity carried out for the obligation to repair the environmental damage to be configured. Also, according to national jurisprudence, such an obligation to repair environmental damage is not subject to statute of limitations[31] and may extend to the board of directors and even the shareholders of the company responsible for the damage.[32]

The case “CVM vs. Vale Directors”[33] is worth noting to illustrate this tendence of cases against the board of directors, despite not being a climate-oriented litigation. Through an administrative sanctioning process, CVM analyzed the responsibility of former Vale S.A. board members in the context of the dam collapse in Brumadinho/MG, which occurred in January 2019. The former CEO was acquitted, whereas the then “Director of Iron Ore and Coal” was convicted due to the violation of the Duty of Diligence (Article 153, Brazilian Corporations Act).

CVM understood that, while the former CEO complied with this duty since he did not receive any warning signs that would have required him to proactively investigate the stability of the dam, the Director remained inactive in the face of alert. Therefore, he was fined R$27,000,000.00, which is a decision considered paradigmatic in the discussion about the responsibility of administrators for social and environmental damages in Brazil.

Cases involving climate damage from illegal deforestation

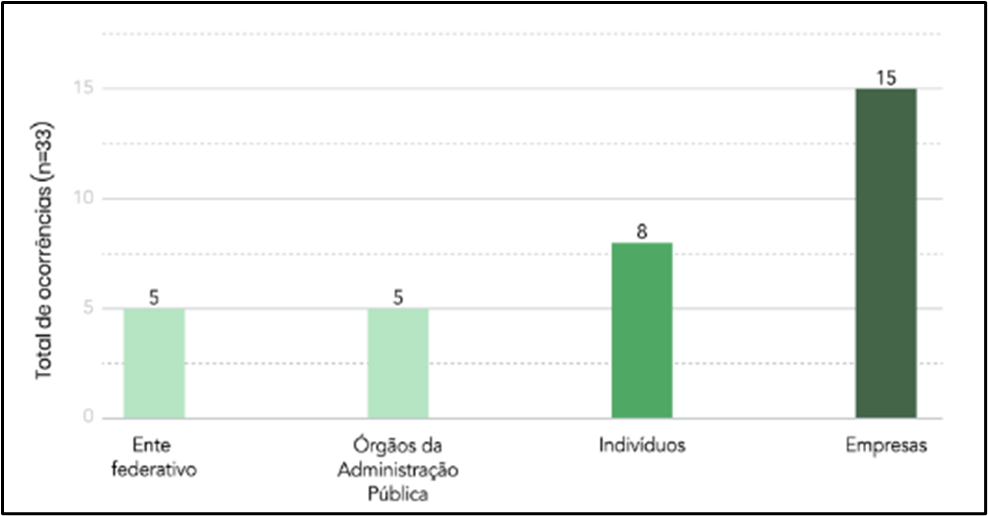

Although it is not yet consolidated in case law, cases have recently begun to emerge in which companies and individuals have been required to repair climate damage. Most of these cases are related to episodes of illegal deforestation that have already been punished with fines in the administrative scope, and now environmental agencies are seeking reparation for the damage in the civil scope. By March 2024, 24 actions had been mapped involving this discussion[34] – most of which were even located in the Legal Amazon region[35]. The overview of the types of entities involved as defendants in these cases is illustrated in Figure 1.

| Figure 1: Civil liability cases: total occurrences by type of liability Source: Moreira, 2024, p. 73[36] |

Among the requests in these cases, the plaintiffs request full compensation for environmental and climate damages[37], including: (i) material damage related to the loss of carbon sinks and environmental degradation until the complete recovery of the area; (ii) irreversible damages, which cannot be reversed; (iii) collective moral damages[38], imposed on society; and (iv) restitution of profits unduly obtained from the polluting activity (illegally obtained profits).[39]

In addition, it is also possible to notice in the cases the tendency to use two methods of calculating climate damage: (i) the social cost of carbon (“SCC”) used by the OECD, which can vary between EUR 60/ton and EUR 120/ton[40] and (ii) the value used by the Amazon Fund of US$ 5.00/ton[41]. Brazilian courts have already applied both values in recent decisions, but there is a certain tendency to prefer the value adopted by the Amazon Fund to the detriment of the value of the SCC, since the judges still consider that there is a lot of scientific uncertainty regarding the valuation used by the OECD method[42].

An emblematic example of these cases is “IBAMA vs. Amazon Madeireira Indústria e Comércio de Madeira EIRELI“.[43] IBAMA requested that the company be compelled to restore a degraded area of 39,412 hectares and to compensate for climate-related damages, calculated using the Social Cost of Carbon (SCC). The environmental agency pointed out that the company kept 2,825.507m³ of wood without legal origin in storage, which would correspond to the suppression of native vegetation in an area equivalent to that mentioned. The wood was seized and valued at 405,000 Brazilian reais, and the company was fined for several environmental infractions, including the presentation of misleading information and the storage of wood from indigenous lands and other unauthorized areas.

On August 15, 2023, a judgment was issued condemning the company to (i) recover the degraded area by submitting and executing a Degraded Area Recovery Plan (“PRAD”), within 60 days after the final and unappealable decision; (ii) in the alternative, pay compensation of 423,363.70 Brazilian reais if recovery is not possible; and (iii) pay compensation of 3,827,228.38 Brazilian reais calculated based on the SCC. Currently, the case is awaiting the judgment of the appeal.

Climate-washing

At the outset, it should be noted that in the Brazilian jurisdiction there are, so far, only two publicly available cases on climate-washing and/or disclosure of climate information, though in many instances disputes may be solved by arbitration and not made public. In summary, they deal with lawsuits filed by the Brazilian Institute for Consumer Protection (“Idec”) against companies in the air transport and mobility sectors with the aim of obtaining greater transparency on emissions offset programs[44]. The cases were filed with the aim of obtaining detailed clarification on the climate information and advertising made by the companies.

In addition, to substantiate the cases, Idec pointed to evidence of a lack of clarity regarding the real benefits of the program, the origin of the carbon credits acquired and the effectiveness of the methods used by the companies. Information and supporting documents were requested on the general conditions of contracting the program, possible irregularities in REDD+ projects, potentially misleading environmental claims and the relationship between price, mileage traveled, and type of fuel used.

On May 13, 2025, the air transport company submitted its responses, and on June 14, 2025, the Public Prosecutor’s Office of the State of São Paulo (“MPSP”) also expressed itself in the records, acknowledging that the purpose of the case had been fulfilled. Currently, the process awaits its archiving, while Idec evaluates the possibility of future judicialization, according to the analysis of the answers provided by the company.

Regarding the other case, on April 24, 2025, the mobility company submitted answers to the questions. Subsequently, on June 25, 2025, the MPSP filed a response in the proceeding, also recognizing that the objective of the case had been fulfilled. On June 26, 2025, the judge dismissed the case.

On November 27, 2025, however, Idec filed a new lawsuit against ‘Gol’, a flight company previously requested to provide information. Idec opted to file an “Ação Civil Pública – ACP” (a type of collective action, similar to Common Law’s Class Actions) based on the information gathered in previous cases[45]. The lawsuit seeks to have the practice legally recognized as greenwashing and requests collective moral damages of BRL 5 million, marking the first time a consumer association has pursued judicial accountability for this practice in Brazil. Also, no decisions were issued by the closure of this chapter.

Regarding Idec main allegations, it argues that (i) the company used tokens issued by a third-party company that got the tokenization of its certified credits prohibited due to risks such as double counting, lack of traceability, and absence of technical proof of retirement and additionality; (ii) the absence of any technical documentation, valid certificates, or transparent information to substantiate Gol’s claims of “neutralizing” flight emissions; and (iii) the misleading nature of the program, which created a false perception among consumers that they were compensating real emissions, when in fact they were purchasing digital assets without proven environmental validity. Idec also requested that Gol be ordered to publish corrective advertising on its official channels and remove unsubstantiated environmental claims from its so-called “green aircraft.”

Climate change and financial institutions

An emblematic example of this type of case is “Conectas vs. BNDES and BNDESPAR“,[46] in which the plaintiff seeks the adoption of concrete measures for financial institutions to align their investment policies with the goals of the Paris Agreement and the National Policy on Climate Change (“PNMC”)[47].

In the lawsuit, the plaintiff argues that the defendants do not have adequate protocols to assess the climate impacts of their investments, which would violate articles 170 and 225 of the Federal Constitution, in addition to the obligations assumed by Brazil at the international level. Conectas argues that the absence of climate criteria in investment decisions compromises the defendants’ public function and represents a failure to comply with the climate due diligence. Among the requests, the presentation of an emissions reduction plan, the installation of a climate situation room and the provision of information on how climate risks are considered in investment, divestment and reinvestment decisions stand out.

The plaintiff also contends that the failure to incorporate climate criteria into investment decisions constitutes a breach of fiduciary duties applicable to the BNDES system. This argument is based on two levels: (i) the duty of the controlling shareholder (Article 116, Brazilian Corporations Act), to ensure that the company fulfills its social function and respects the rights and interests of the community; and (ii) the duty of administrators (Article 154, Brazilian Corporations Act) to satisfy the requirements of the public interest and the company’s social function. According to the plaintiff, these obligations require BNDES and its wholly-owned subsidiary BNDESPAR to integrate climate considerations into their investment and divestment strategies, as part of their stewardship responsibilities and in alignment with the Social, Environmental and Climate Responsibility Policy (“PRSAC”) and PNMC’s objectives.

In their defense, BNDES and BNDESPAR claimed that their credit and investment decisions are of a private nature and that they already adopt internal policies and ESG protocols, such as the Social, Environmental and Climate Responsibility Policy (“PRSAC”)[48] and the “NDC Panel”.

In August 2022, a decision was issued denying the urgent relief requested by the plaintiffs on the grounds that the urgency of the requests was not proven. Currently, the case is still active and awaits the start of the investigative phase or the holding of a conciliation hearing between the parties.

[1] ‘Federal Constitution’ <https://www.planalto.gov.br/ccivil_03/constituicao/constituicao.htm> Accessed on July 25, 2025.

[2] Article 170. The economic order, founded on the valorization of human work and free enterprise, aims to ensure a dignified existence for all, according to the dictates of social justice, observing the following principles: (…) VI – defense of the environment, including through differentiated treatment according to the environmental impact of products and services and their processes of preparation and provision;

[3] ADPF 708 – Judgment rendered in July 2022. Available at: < https://portal.stf.jus.br/processos/downloadPeca.asp?id=15353796271&ext=.pdf>. Accessed on September 01, 2022.

[4] Article 225. Everyone has the right to an ecologically balanced environment, a good for the common use of the people and essential to a healthy quality of life, imposing on the Government and the community the duty to defend and preserve it for present and future generations

[5] ‘Law No. 6,404/76′ <https://www.planalto.gov.br/ccivil_03/leis/l6404consol.htm> Accessed on July 25, 2025.

[6] The shareholder value primacy theory concerns the company’s vision with the sole objective of returning value to its shareholders. For more information Gordon Smith, D ‘The Shareholder Primacy Norm’ (23 J. CORP. L., 277, 1998) <https://digitalcommons.law.byu.edu/faculty_scholarship/27/> accessed on July 31, 2025.

[7] Pargendler, Mariana ‘Corporate Law in the Global South: Heterodox Stakeholderism’ (47 Seattle U.L. REV. 535 2025) <https://digitalcommons.law.seattleu.edu/sulr/vol47/iss2/7/> accessed on 5 October 2025.

[8] Under Brazilian law, companies may be incorporated under different legal forms, such as limited companies (ex. “sociedade em conta de participação”, “sociedade limitada” etc), both of them are regulated by the Brazilian Civil Code. In addition, there are also anonymous companies “sociedades anônimas”, which are regulated by the Brazilian Corporations Act. Companies that are “sociedades anônimas” may be either publicly-held (listed) or closely-held (unlisted) (Article 4, Brazilian Corporations Act). Among these types, the most common forms opted by Brazilian companies are “sociedades limitadas” and “sociedades anônimas” (listed and unlisted). See ‘Brazilian Civil Code’ <https://www.planalto.gov.br/ccivil_03/leis/2002/l10406compilada.htm> and ‘Brazilian Corporations Act’ <https://www.planalto.gov.br/ccivil_03/leis/l6404consol.htm> accessed on December 04, 2025.

[9] ‘Federal Decree No. 12.705/2025’ <https://www.planalto.gov.br/ccivil_03/_ato2023-2026/2025/decreto/D12705.htm> accessed on December 04, 2025.

[10] CBPS Technical Pronouncement 01 – General Requirements for Disclosure of Financial Information Related to Sustainability. Available at: < https://s3.sa-east-1.amazonaws.com/static.cpc.aatb.com.br/Documentos/655_pronunciamento.pdf> Accessed on September 1, 2025.

[11] CBPS Technical Pronouncement 02 – Climate-Related Disclosures Correlation to the International Sustainability Standard – IFRS S2. Available at: < https://s3.sa-east-1.amazonaws.com/static.cpc.aatb.com.br/Documentos/658_pronunciamento.pdf> Accessed on September 1, 2025.

[12] https://conteudo.cvm.gov.br/legislacao/resolucoes/anexos/200/resol217.htm

[13] https://conteudo.cvm.gov.br/legislacao/resolucoes/anexos/200/resol218.htm

[14] CVM Resolution No. 59 < https://conteudo.cvm.gov.br/legislacao/resolucoes/resol059.html> Accessed on July 21, 2025.

[15] CVM Resolution No. 193 <https://conteudo.cvm.gov.br/legislacao/resolucoes/resol193.html> Accessed on July 21, 2025.

[16]CVM Resolution No. 217 < https://conteudo.cvm.gov.br/export/sites/cvm/legislacao/resolucoes/anexos/200/resol217.pdf> Accessed on July 31, 2025.

[17]CVM Resolution No. 218 < https://conteudo.cvm.gov.br/export/sites/cvm/legislacao/resolucoes/anexos/200/resol218.pdf> Accessed on July 31, 2025.

[18]CVM Resolution No. 219 < https://conteudo.cvm.gov.br/export/sites/cvm/legislacao/resolucoes/anexos/200/resol219.pdf> Accessed on July 31, 2025.

[19]CVM Resolution No. 227 < https://conteudo.cvm.gov.br/export/sites/cvm/legislacao/resolucoes/anexos/200/resol227.pdf> Accessed on July 31, 2025.

[20] According to the amendment introduced by CVM Resolution No. 227, entities must apply the ISSB standards in their original English version until the CBPS completes the internalization process and the standards are approved by the CVM (Article 1, paragraph 1).

[21] ‘Brazil is the 1st country in the world to adopt a report on sustainability-related financial information issued by the ISSB’ <https://www.gov.br/cvm/pt-br/assuntos/noticias/2023/brasil-e-1o-pais-no-mundo-a-adotar-relatorio-de-informacoes-financeiras-relacionadas-a-sustentabilidade-emitidas-pelo-issb> Accessed on July 21, 2025.

[22] Abrasca ‘Abrasca presents research on IFRS S1 and S2 at KPMG event’ <https://abrasca.aatb.com.br/noticias/sia-cia-1727-abrasca-apresenta-pesquisa-sobre-sobre-ifrs-s1-e-s2-em-evento-da-kpmg> accessed on July 30, 2025.

[23] ‘Law No. 15.042/2024’ <https://www.planalto.gov.br/ccivil_03/_ato2023-2026/2024/lei/L15042.htm> accessed on July 28, 2025.

[24] ‘CMN Resolution No. 4,943/2021’ <https://www.bcb.gov.br/estabilidadefinanceira/exibenormativo?tipo=Resolu%C3%A7%C3%A3o%20CMN&numero=4943> accessed on December 05, 2025.

[25] ‘CMN Resolution No. 4,945/2021’ <https://www.bcb.gov.br/estabilidadefinanceira/exibenormativo?tipo=Resolu%C3%A7%C3%A3o%20CMN&numero=4945> accessed on December 05, 2025.

[26] ‘BCB Resolution No. 139/2021’ <https://www.bcb.gov.br/estabilidadefinanceira/exibenormativo?tipo=Resolu%C3%A7%C3%A3o%20BCB&numero=139> accessed on December 05, 2025.

[27] ‘BCB Normative Instruction No. 153/2021’ https://www.bcb.gov.br/estabilidadefinanceira/exibenormativo?tipo=Instru%C3%A7%C3%A3o%20Normativa%20BCB&numero=153 accessed on December 05, 2025.

[28] ‘BCB Resolution No. 151/2021’ <https://www.bcb.gov.br/estabilidadefinanceira/exibenormativo?tipo=Resolu%C3%A7%C3%A3o%20BCB&numero=151> accessed on December 05, 2025.

[29] ‘Law No. 9.605/1998’ <https://www.planalto.gov.br/ccivil_03/leis/l9605.htm> accessed on July 29, 2025.

[30] ‘Law No. 6.938/1981’ <https://www.planalto.gov.br/ccivil_03/leis/l6938.htm> accessed on July 28, 2025.

[31] According to Theme 999 of the Federal Supreme Court, “civil reparation of environmental damage is not subject to statute of limitations”, due to the recognition that reparation of damage to the environment is an unavailable fundamental right and, therefore, reparation of environmental damage is not subject to statute of limitations.

[32] Considering the unavailable nature of environmental protection, as well as the principles of full reparation and polluter pays, article 4 of Law No. 9,605/1998 guarantees the possibility of disregarding the legal entity when its personality is an obstacle to the compensation of damages caused to the environment, thus enabling the reach of shareholders of the company causing environmental damage. In this sense, article 3 of Law No. 6,938/1981, when defining the polluting entity, includes the individual or legal entity responsible, directly or indirectly, for an activity that causes environmental degradation. Thus, individuals or legal entities that finance, contract or benefit from potentially polluting activities, without adopting control or prevention measures, can be held liable as indirect polluters, especially when there is a breach of the duty of environmental diligence.

[33] ‘CVM conclui julgamento que analisa dever de diligência de ex-diretores da Vale S/A e multa em R$ 27 milhões Diretor de Ferrosos e Carvão da companhia’ <https://www.gov.br/cvm/pt-br/assuntos/noticias/2024/cvm-conclui-julgamento-que-analisa-dever-de-diligencia-de-ex-diretores-da-vale-s-a-e-multa-em-r-27-milhoes-diretor-de-ferrosos-e-carvao-da-companhia> accessed on December 04, 2025.

[34] Moreira, Danielle (coord.), ‘Panorama da Litigância Clima no Brasil’ (Rio de Janeiro, PUC-Rio, 2024, p. 73) <https://juma.jur.puc-rio.br/_files/ugd/a8ae8a_98130c7a71f542e1949db1b2d8646e35.pdf> accessed on July 29, 2025.

[35] The “Legal Amazon” comprises the Brazilian states: Acre, Amazonas, Amapá, Mato Grosso, Pará, Roraima and Rondônia, Tocantins and part of Maranhão. See more information about the Legal Amazon <https://www.gov.br/sudam/pt-br/acesso-a-informacoes/institucional/legislacao-da-amazonia> accessed on September 03, 2025.

[36] From right, to left, read: “Federative Entities”; “Public Agencies”; “Individuals”; and “Companies”. In addition, the total number in this graph is greater than the number of cases, as there are cases with more than one defendant with different natures.

[37] There is still no legal provision for the concept of “climate damage”, so it is still under construction in the Brazilian legal regime. On the one hand, scholars treat climate damage as a kind of environmental damage and define climate damage as “the damage directly done to the legal good climate system” (Rosa, Rafaela ‘Climate Damage: concept, assumptions and accountability’ São Paulo: Tirant Lo Blanch, 2023, p. 35 and p. 331). On the other hand, the National Council of Justice (“CNJ”) itself published Resolution No. 433/2021, which determines that Brazilian judges must include in the assessment of environmental damage the impacts on (i) global climate change, (ii) diffuse damage to affected peoples and communities, and (iii) the deterrent effect on environmental externalities caused by polluting activity (Art. 14). ‘ CNJ Resolution No. 433/2021’ <https://atos.cnj.jus.br/atos/detalhar/4214> accessed on September 03, 2025.

[38] There is also no legal provision for the concept of “collective moral damage”. Even so, the case law of the STJ provides seven criteria for the determination of collective moral damage due to environmental damage: (i) the need for unfair conduct that is offensive to nature; (ii) objective assessment of the damage; (iii) presumption of intolerable injury and reversal of the burden of proof; (iv) independence of material recomposition; (v) conjunctural assessment and joint and several liability; (vi) adequacy of the amount of compensation (quantum debeatur) based on the peculiarities of the case (e.g., the offender’s contribution, the offender’s socioeconomic situation, the extent and perpetuity of the damage, the seriousness of the fault and the benefit obtained from the unlawful act); and (vii) location of the damage in biomes considered as national heritage by the Federal Constitution. See more information on the topic <https://www.mattosfilho.com.br/unico/dano-diretrizes-ibama-stj/> accessed on September 03, 2025.

[39] Moreira, Daniele. Ibid., p. 82.

[40] OECD ‘Pricing Greenhouse Gas Emissions 2024: Gearing up to bring emissions down’ (OECD Series on Carbon Pricing and Energy Taxation, 2024, p. 19) <https://www.oecd.org/content/dam/oecd/en/publications/reports/2024/11/pricing-greenhouse-gas-emissions-2024_173c47f4/b44c74e6-en.pdf> accessed July 29, 2025.

[41] Brazil ‘Technical Note No. 1371/2024-MMA’ (2024) <https://www.fundoamazonia.gov.br/export/sites/default/pt/.galleries/documentos/ctfa/Nota_Tecnica_12a_2024.pdf> accessed on July 29, 2025.

[42] “Despite the numerous divergences that still hover on the subject (the news of the creation of a Working Group by the National Council of Justice, through Ordinance No. 176/2023, which has the scope of defining guidelines for the quantification of environmental damage), considering that the amount attributed in the initial petition is considerably lower than that obtained in an OECD study, considering that there was no controversy in the record on this point (article 374, III, of the Code of Civil Procedure) and also considering the principle of periodic payment (article 492 of the Code of Civil Procedure), I adopt the value of US$5.00 per ton of CO2e to fix the climate damage” (ACP No. 1015022-84.2021.4.01.3200, Judge Rodrigo Antônio Mello, 7th Federal Environmental and Agrarian Court of SJAM, September 20, 2024).

[43] Public Civil Action No. 1000364-26.2019.4.01.3200. For more information on the case <https://litigancia.biobd.inf.puc-rio.br/visualizacao_caso/869/0/> accessed on July 29, 2025.

[44] The cases are ‘Idec vs. Localiza’ <https://litigancia.biobd.inf.puc-rio.br/visualizacao_caso/993/0/> and ‘Idec vs. Gol’ <https://litigancia.biobd.inf.puc-rio.br/visualizacao_caso/1011/0/> accessed on December 04, 2025.

[45] ‘Idec entra com ação contra Gol por greenwashing’ <https://idec.org.br/release/idec-entra-com-acao-contra-gol-por-greenwashing?fbclid=PAb21jcAOer8xleHRuA2FlbQIxMQBzcnRjBmFwcF9pZA81NjcwNjczNDMzNTI0MjcAAadEbVIFa7JKCW92Pf-WuZHKDmKDsDBo8-0NuTU4r7Urb-nEcz_0p8KgVpD2OQ_aem_vHnWeh59uooNcdc-kd73eA> accessed on December 05, 2025.

[46] ACP No. 1038657-42.2022.4.01.3400. For more information on the case “Conectas vs. BNDES and BNDESPAR” <https://litigancia.biobd.inf.puc-rio.br/visualizacao_caso/340/0/> accessed on July 31, 2025.

[47] ‘Law No. 12.187/009’ <https://www.planalto.gov.br/ccivil_03/_ato2007-2010/2009/lei/l12187.htm> accessed on July 31, 2025.

[48] ‘PRSAC BNDES’ <https://www.bndes.gov.br/wps/portal/site/home/desenvolvimento-sustentavel/o-que-nos-orienta/prsac-e-seus-instrumentos/politica-responsabilidade-social-ambiental-climatica/> accessed on July 31, 2025.